Task 4: Record depreciation

If you depreciate your assets at the end of the financial year, make this step a part of your end-of-year routine. Consult your tax adviser or accountant for information on when to depreciate your assets.

Your company’s vehicles and equipment lose value each year. Part of the cost of vehicles and equipment can be allocated as an expense to your company each year you benefit from their use. The allocation of the cost of a piece of equipment over its useful life is called depreciation.

There are several methods of depreciation. Consult your accountant to see whether you should be depreciating vehicles and equipment and, if you should, which method is best for you.

Your software doesn’t calculate depreciation automatically, but you can record your depreciation figures quickly with a journal entry.

|

1

|

Create a new asset account for each type of asset you depreciate. Add the words ‘Accum Dep’ (for Accumulated Depreciation) at the end of each new account name. Give the new account a number that allows it to come directly after its corresponding asset account in the accounts list. For more information on creating a new account, see Set up accounts.

|

In the following example, we have a header account, Vehicles, numbered 1‑1500, and a detail account, Vehicles Original Cost, numbered 1‑1510. We have created a new asset account called Vehicles Accum Dep, numbered 1‑1520. Notice that the header account shows the current book value of the vehicles.

|

2

|

Create a new expense account. You may want to call it Depreciation.

|

|

3

|

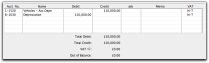

Once you’ve determined your depreciation amounts, make journal entries to credit the new accumulated depreciation asset accounts and debit the new depreciation expense account. The accumulated depreciation asset accounts will always have a negative balance to show a reduction in the value of the depreciable assets.

|